The era of software growth is giving way to physical breakthroughs. To fund the next century, venture capital must learn to track steps, not revenue.

By Ritu Verma

2026

By Ritu Verma

2026

In 1972, Stephen Jay Gould and Niles Eldredge were studying rocks [1]. Darwin had predicted that species change gradually - accumulating small improvements over long periods, which should have left a trail in the rock. But the fossils told a different story. Species would sit essentially unchanged for millions of years. Then, in a geological blink, transform. Gould and Eldredge named this Punctuated Equilibrium. The quiet stretches were doing the work that makes the next jump possible.

As a former physicist with over a decade of investing in science, I was surprised by how perfectly this biological framework describes deep tech value creation. I have sat through these plateaus—wondering if the gas connection for a pilot plant will ever come through, or if endless negotiations with a critical customer will finally bear fruit. A deep tech company does not grow continuously – its value moves in sudden steps, separated by long, flat plateaus where the hardest-and most misunderstood-work gets done. The companies in these flat stretches will rewrite how the world eats, powers itself, and heals.

Those plateaus are where the next century gets built.

The next massive waves of value creation will not be built on code, but on the physical infrastructure of human survival: chemistry, biology, advanced materials, and energy. Agriculture will be rewritten by synthetic biology. Logistics will be upended by novel energy storage. Heavy manufacturing will be redefined by advanced metallurgy. Every one of these companies will climb the steps. But you cannot underwrite physical breakthroughs using software metrics.

Software investors track revenue. Deep tech investors track steps. We call this approach Staircase Capital.

While every deep tech company climbs this same physical staircase shape – the trigger differs by industry, the step timing by technology, the step height by market.

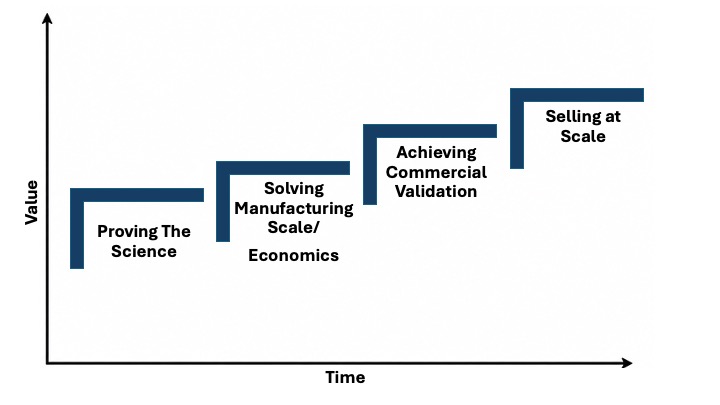

Fig. 1 The journey from IP filing to commercial scale across four deep tech sectors.

[1] "Punctuated Equilibria: An Alternative to Phyletic Gradualism" in Models in Paleobiology, 1972, edited by T.J.M. Schopf

The flat stretches between steps are the hardest part of this asset class for everyone — investors, founders, and employees alike. From the outside it looks like a company going nowhere. Money is being spent. There are no press releases. The metrics that signal progress at a software company — revenue, user acquisition, viral growth — are either absent or entirely the wrong things to measure.

I have sat through these flat stretches from both sides. I have been in board meetings where the deck looks identical to last quarter because an entire team is waiting on for a piece of equipment for a pilot plant. And I have been in fundraising meetings where the growth investor across the table searches frantically for a SaaS inflection that will never come. The meeting ends. The misunderstanding repeats across companies.

The capital is available. The framework to deploy it is not.

What matters here is different: is the yield improving, is the regulatory feedback constructive, is the team solving the right problem.

It is where scale-up manufacturing, real world trials, regulatory clearances, partnerships get solved. The reason these valuation jumps appear to happen "overnight" is that each step represents the elimination of a binary risk. When a company proves its material can scale consistently or passes an FDA hurdle, a massive risk category instantly drops to zero- triggering the leap in valuation.

I learnt about misjudging the flat stretch first hand. In 2008, I was evaluating lithium battery companies globally. A123, an MIT spinout, had everything an investor could want: world-class science, prestigious pedigree, and government backing. In contrast, BYD was a scrappy Chinese company with none of the classical signals of a winner. While we didn’t end up deploying capital , I continued to follow the companies. By 2012, A123 filed for bankruptcy after burning through $3 billion. Meanwhile, BYD continued its march to become the world’s largest electric vehicle manufacturer. Looking back, Charlie Munger famously described BYD’s founder as "Edison and Welch combined" - someone who could both invent and manufacture. A123 could only do the former. Investors failed to distinguish between a plateau that was working (where manufacturing economics were being quietly solved) and one that was fundamentally broken, leading to a massive loss.

This is the first in a series. Each piece that follows goes deeper - sector by sector, technology by technology, unpacking what has already played out in order to understand what comes next and particularly how this is playing out in India, where we invest.

Once you understand the staircase, the traditional venture playbook goes out the window. Surviving this asset class requires drawing a sharp, non-negotiable line in the sand before deploying a single dollar

When the market cannot distinguish between an unproven science experiment and a scaling factory, it misprices both. That mispricing is where fortunes are made. In India, this mispricing is compounded. Global and local capital routinely overlooks deep tech in India. The discount is deeper and more persistent. The information edge available to an investor who has spent a decade on the ground is correspondingly larger.

You do not have to run the whole race - but you need to know your leg

.png)

The question I get asked most often: Can a traditional venture fund actually make money in deep tech?

The pushback always centers on the word patient. Critics argue that because deep tech requires long horizons, standard 10-year closed-end funds are structurally excluded from making money-leaving the asset class entirely to capital that doesn’t have fixed timelines.

My answer: It depends on whether you understand which leg of the race you are running.

Nobody funds these companies from inception to global dominance. Deep tech is a relay race. The scientist has the idea and grant capital supports it; the first investor proofs the science; a second backs the scale-up; a third finances the commercial launch. By the time a retail investor buys shares on a public exchange, four or five distinct groups of capital have already generated liquidity and passed the baton.

.jpg)

Fig 2. The early check: documented returns from early investors [2]. The size of bubbles represent the MOIC for the return. BCG's analysis of over 2,000 deep tech companies found that deep tech and traditional VC funds deliver near-identical IRRs — 25% versus 26% respectively [3].

[2] Returns are estimates based on publicly available data. All examples represent realised or part-realised exits for early-stage investors. Sources: public filings, company announcements, Ankur Capital estimates. [3] BCG: An Investor's Guide to Deep Tech, Boston Consulting Group, November 2023

These returns in deep tech investments are the logical outcome of entering before a specific trigger fires, capturing the jump, and handing off. To read the quiet between the steps, we filter every deal through four ruthless lenses:

So can a venture fund make money in deep tech? Yes. But not by being patient, by being precise.

This staircase is not theoretical. It is being built right now in the most hyper-competitive capital environment on earth: India.

For a decade, I have defended this reality in LP meetings, co-investor conversations, and rooms where the phrase "Indian deep tech" was met with polite skepticism. The critics always point to the same missing elements: the exits aren’t there yet, and the long-term track record isn't established. But those rooms are looking backward. They are missing the pipeline. When we mapped our own deal flow at Ankur, deep tech accounted for more than 50% of the companies we saw—up from less than 5% just five years ago.

We are still writing the early chapters of how Staircase Capital plays out here. Indian labs are producing world-class breakthroughs across advanced materials, synthetic biology, and space missions, fueled by foundational grant schemes like BIRAC and ANRF. But what makes this ecosystem truly revolutionary isn't just the science.

India possesses a structural unfair advantage: our flat stretches simply cost less to sit in.

Globally, moving from proven science to commercial scale requires a massive, dilutive $20 million Seed-to-Series A jump before real market validation exists. In India, that exact same journey is achieved through far more economical steps.

Take one of our synthetic biology portfolio companies. They are currently sitting in a plateau—their manufacturing yield is proven, their first commercial customer has paid, and they are waiting on large off-take contracts. They achieved all of this with about one-fifth the capital of their global counterparts.

This capital efficiency isn’t just driven by lower engineering talent costs or cheaper fabrication. India offers a high-velocity testbed: an economy dense with smaller, hungry businesses willing to adopt new technologies if—and only if—the economic utility is undeniable. Proving your science under the brutal margin discipline of an Indian B2B customer is a harder, more valuable proof than any cleanroom lab result. Indian companies that clear this bar have already solved a commercial scale reality most global competitors never face.

At the same time, policy momentum is accelerating. The government is simultaneously funding the science, building the industrial clusters, and procuring the output—anchored by a massive $12 billion commitment through the RDI Scheme. Few global markets offer all three components simultaneously.

Still, there are distinct challenges.

The domestic capital stack is thin, as the majority of local investors are still conditioned to back software. The investors we have approached have been unwilling to underwrite without revenue or have limited their checks to tiny numbers to control risk.

Furthermore, global entry costs do not compress: navigating FDA approvals, securing CE marks, and executing international business development cost the same regardless of where the technology was built. To survive, Indian founders must build cross-border bridges long before they actually need them.

This is where the true rerating opportunity lies: backing Indian-origin technology at a price that reflects local capital scarcity, rather than the global quality of the innovation.

This playbook has been tested elsewhere. Take Israel: a tiny domestic footprint paired with a powerhouse science base, aggressive government validation, a high-velocity testing environment, and a global outlook from day one. Many entrepreneurs have leveraged that to build multi-billion-dollar global champions. Israel proves a fundamental architectural truth: the geography of building does not have to match the geography of selling.

India possesses all of Israel’s core ingredients, plus one unfair advantage: a massive domestic market capable of generating genuine commercial scale before a global market rollout.

I have spent years working closely with India's deep tech pioneers—brainstorming through the bottlenecks, celebrating the leaps, and talking into the night about the frustrations. As they climb this staircase, I am entirely convinced they will build globally competitive giants.

The data backs up that conviction: patent filings have more than doubled to cross 100,000, space funding has surged 235% since privatization, and nearly a billion dollars has poured into techbio [4]. The pipeline is real. The companies climbing these staircases right now are rewriting how human civilization runs—from clean energy and early-disease diagnostics to advanced materials and equitable compute.

But to get them there, the next decade needs three groups of people to step up.

If you are a founder willing to climb the staircase, pay attention to the factors beyond the science. Make sure you surround yourself with the right commercial and engineering talent to build the next steps. If you are an investor, look closer at these plateaus. Pushing capital into the wrong step, or failing to understand the quiet work happening beneath the surface, is exactly how funds lose money in this asset class. And most importantly—if you are talent that has spent time in a large company, a GCC, or a government lab—take the risk. The operational learnings you carry from those institutions are exactly what deep tech founders desperately need and cannot easily hire. Bring them. Put them to work.

Whether those breakthroughs reach seven billion people in the next twenty years—or wait another generation—depends entirely on whether the capital that finds them can read the staircase.

The deep tech investor's job is to read that quiet correctly and know exactly when the world is about to jump.

[4] Ankur Capital India Deep Science Tech Report 2025

Registered Corporate Office

Ankur Fincon Management Pvt Ltd

Unit 5 Jetha Compound,

Byculla (E),

Mumbai 400027